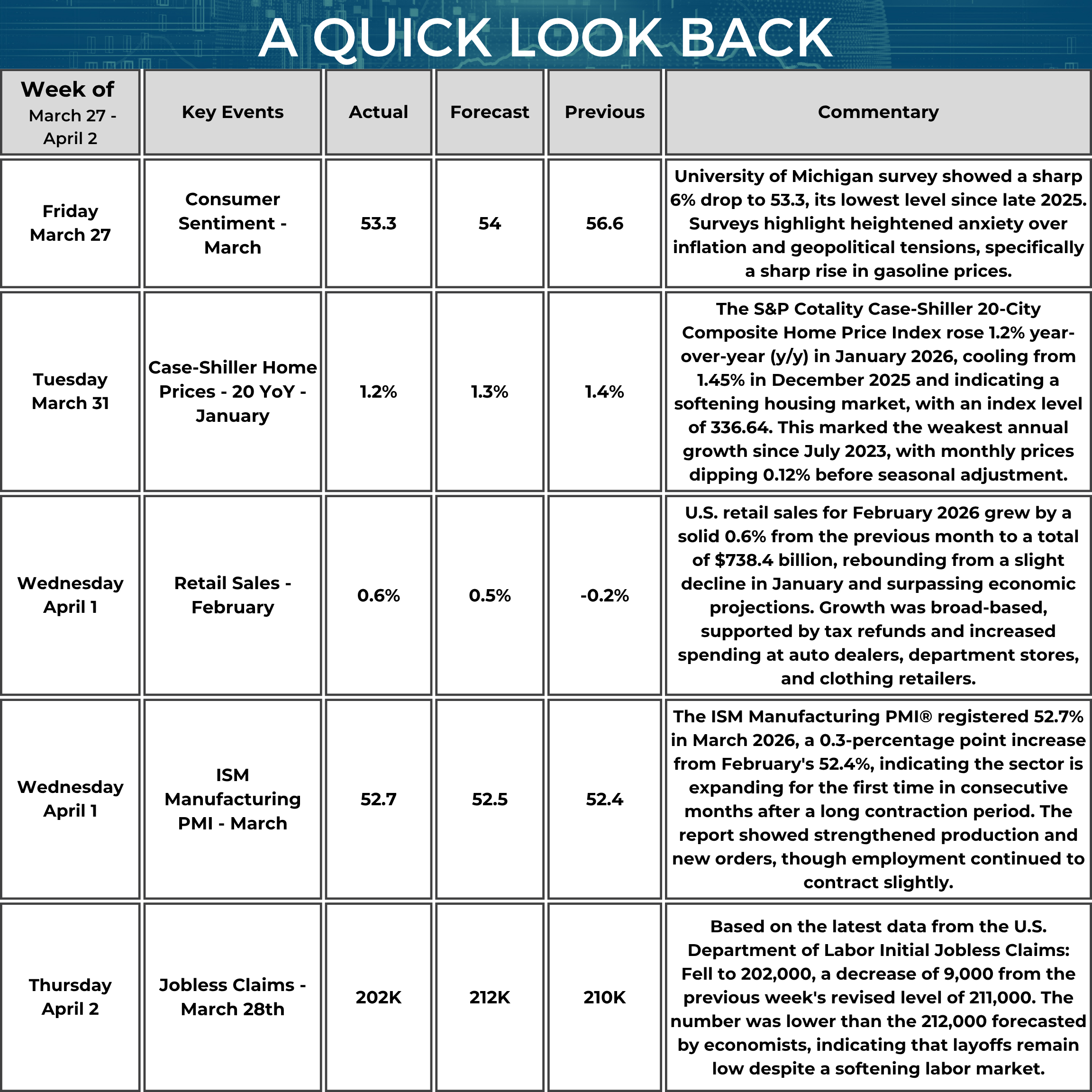

Welcome to our Market Update, written by our very own Capital Market experts. This blog is designed to give you a glance into the most important market events happening this week.

Market Commentary:

Mortgage rates climbed steadily through the end of March, reversing the softer trend seen earlier in the month. By March 27, 30‑year fixed rates were already pushing into the mid‑6% range, and they continued rising day by day as inflation concerns, higher oil prices, and geopolitical tensions pushed Treasury yields upward. Even without a new Fed rate move, markets priced in fewer future rate cuts, which kept mortgage rates elevated. This created a more cautious environment for borrowers, with many delaying locks or revisiting affordability as monthly payments increased. Sellers are gradually adjusting price expectations, while buyers are recalibrating budgets and negotiating more aggressively.

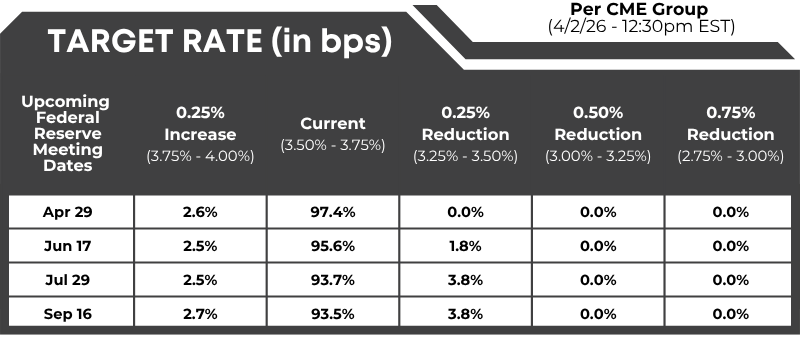

FedWatch: Target rate (in bps) possibilities, according to the CME Group (as of 04/02/2026 – 12:00 PM EST):

Consumer Confidence Climbs Despite Oil Price Surge:

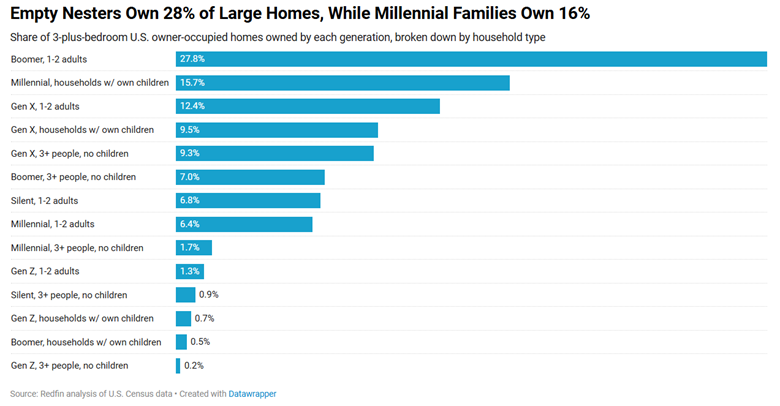

The Great Housing Mismatch: Empty Nesters Own 28% of the Nation’s Large Homes, Millennial Families Own 16%:

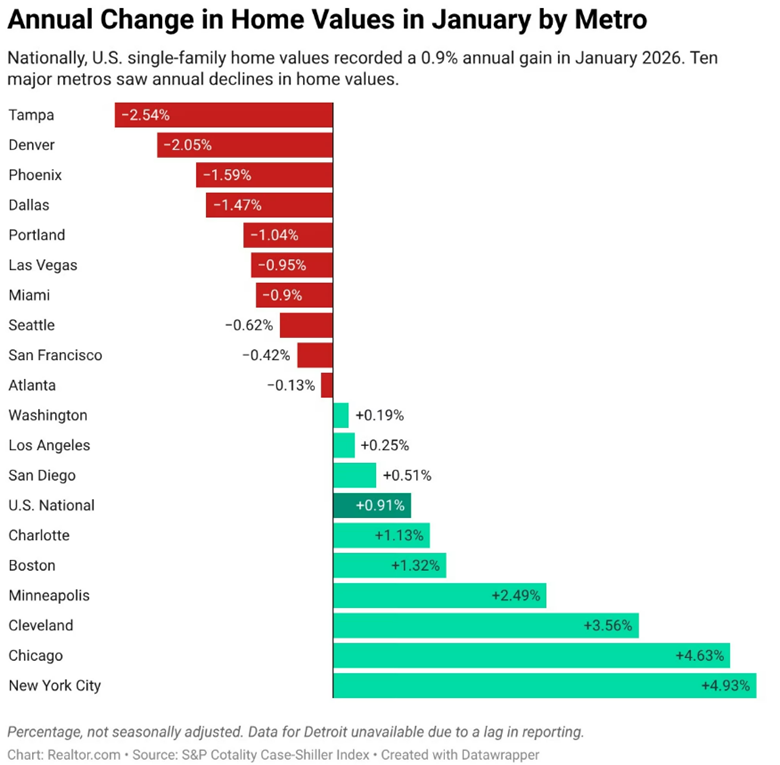

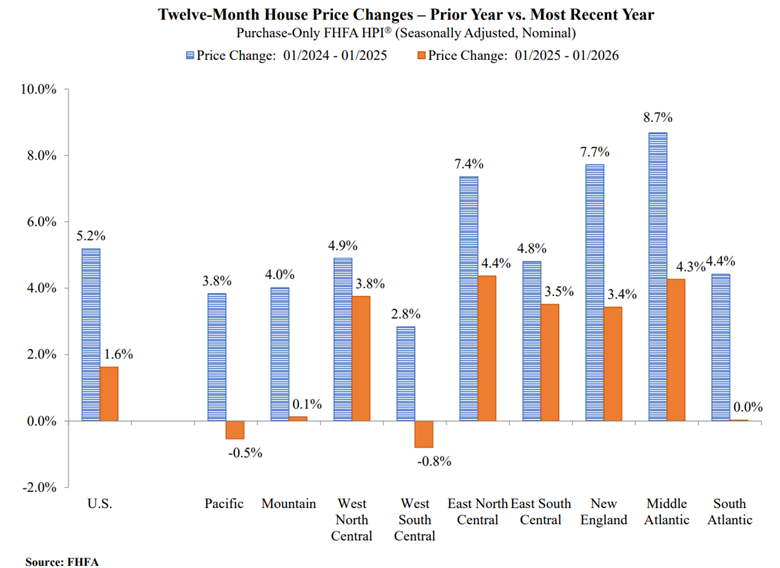

Home Value Growth Slows Dramatically in January:

Women’s Month Fun Facts:

- Single women make up about 21% of homebuyers, compared to about 9% for single men.

- The median age of single women homeowners is about 63, compared with 57 for single men.

- According to NAR, single women have a higher homeownership rate than single men in 57% of U.S. metro areas.

- Women 35 to 44 also saw an increase in homeownership, from 36% to 40%.

- Widowed women remain the most likely to own homes, with a homeownership rate of about 73%.

- Homeownership among divorced women climbed from 55% to 60%, separated women from 33% to 39%, and never-married women from 30% to 34%.

Insignificant Impact:

Looking back over the past ten oil price shocks dating back to 1986, the average increase in the price per barrel is 115.5%. Before the shock, Y-o-Y core PCE inflation has averaged 3% and at the end of the shock Y-o-Y core PCE has averaged 3%, no change! What happens is food and energy prices skyrocket but consumers buy less other stuff, as real incomes sink, driving those prices down. - Elliot Eisenberg, Economist

News You Can Use:

· Private sector hiring totaled 62,000 in March, better than expected, ADP says

· Fed's Schmid: Inflation is the more salient risk for the economy | investingLive

· Powell sees inflation outlook in check, no need to hike rates because of oil shock

· Today's Case-Shiller: Growth Slows to +0.9% Annual Gain

· Housing market demand is holding, but pricing gaps are breaking deals

· Single Women Outnumber Single Men When It Comes to Homeownership

*Communication is intended for Industry Professionals only and not intended for Consumer Distribution

Interest rate and annual percentage rate (APR) are based on current market conditions as of 04/02/2026, are for informational purposes only, are subject to change without notice and may be subject to pricing add-ons related to property type, loan amount, loan-to-value, credit score and other variables. Estimated closing costs used in the APR calculation are assumed to be paid by the borrower at closing. If the closing costs are financed, the loan, APR and payment amounts will be higher. Contact us for details. Additional loan programs may be available. Accuracy is not guaranteed, and all products may not be available in all borrower's geographical areas and are based on their individual situation. This is not a credit decision or a commitment to lend. actual interest rate, APR, and payment may vary based on the specific terms of the loan selected, verification of information, your credit history, the location and type of property, and other factors as determined by Prosperity Home Mortgage, LLC. Not available in all states. Rate is as of 04/02/2026 and is subject to change at any time without notice. Opinions, estimates, forecasts, and other views contained in this document are those of Freddie Mac’s economists and other researchers, do not necessarily represent the views of Freddie Mac or its management, and should not be construed as indicating Freddie Mac’s business prospects or expected results. Although the authors attempt to provide reliable, useful information, they do not guarantee that the information or other content in this document is accurate, current, or suitable for any particular purpose. All content is subject to change without notice. All content is provided on an “as is” basis, with no warranties of any kind whatsoever. Information from this document may be used with proper attribution.

.png)

.png)