This Market Update is written by our Capital Market specialists each week to bring you insight into what's happening in the market and how it may affect mortgage rates and real estate trends.

Market Commentary:

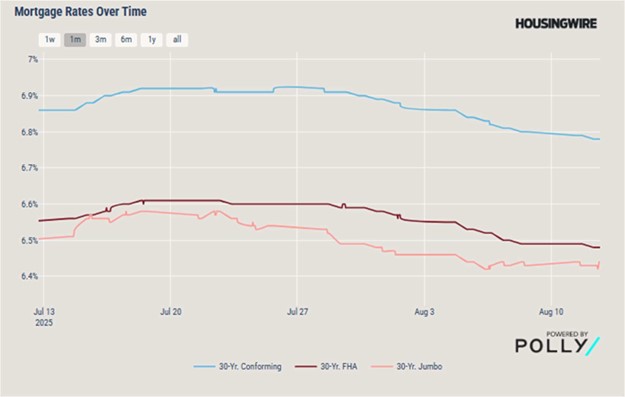

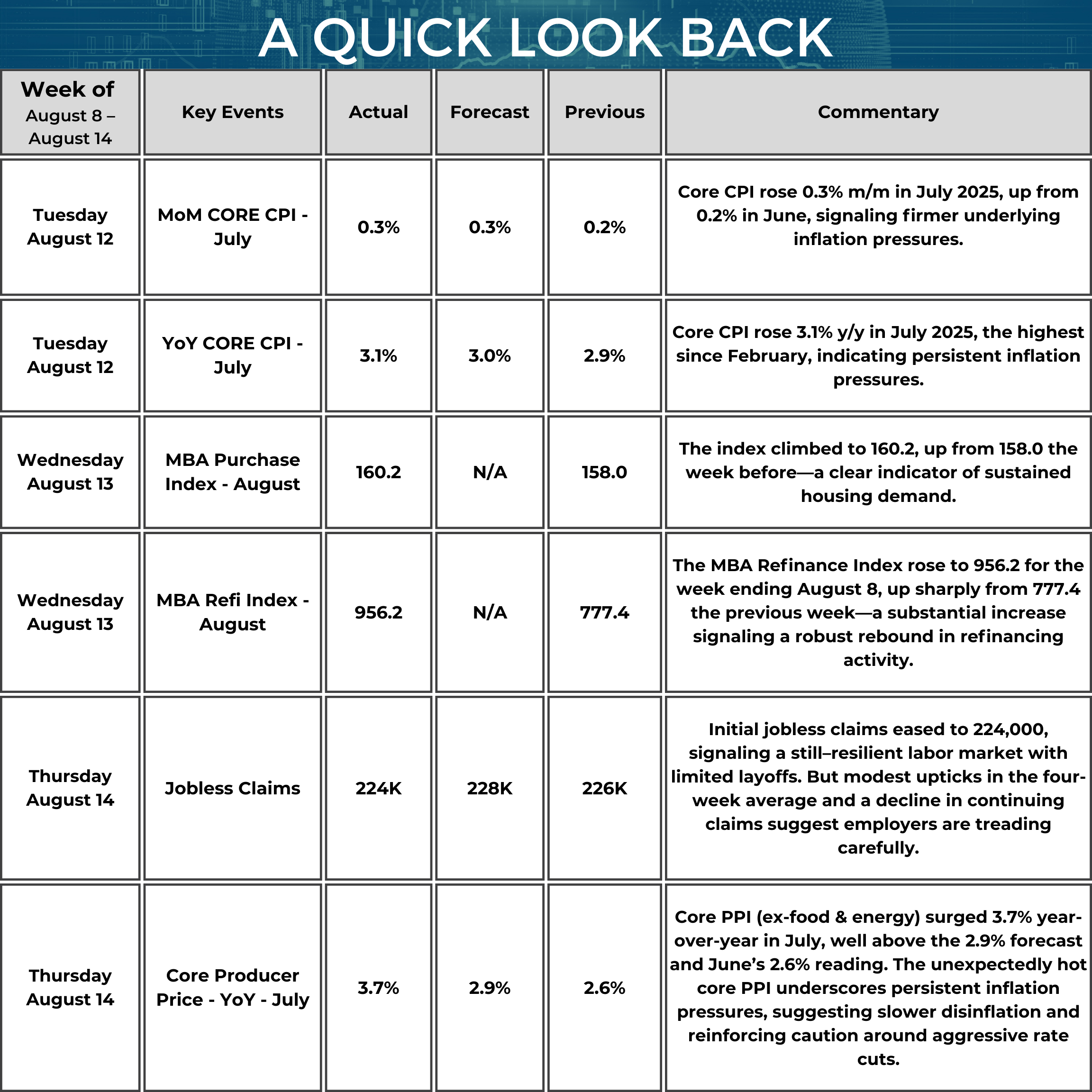

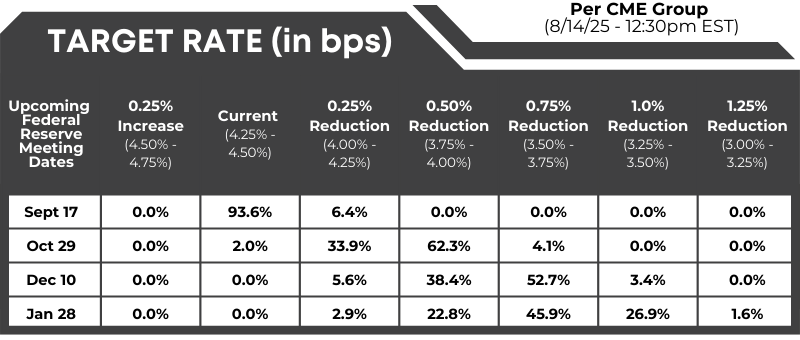

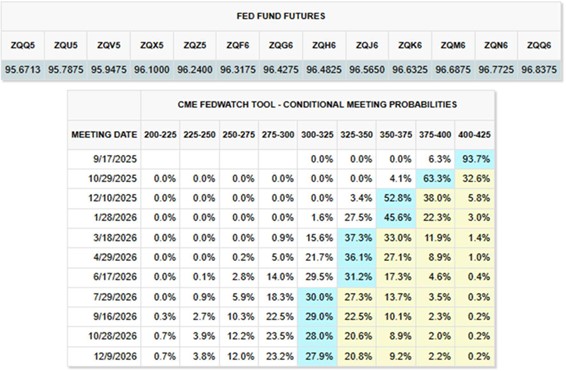

Mortgage rates declined over the week of August 8–14, with the average 30-year fixed falling to 6.76%, its lowest level since early April. This drop fueled a surge in refinance activity, with the MBA Refinance Index jumping to 956.2 from 777.4 the prior week. The refinance share of mortgage activity increased to 46.5% of total applications from 41.5% the previous week. Overall mortgage applications rose 10.9%. Purchase applications posted a smaller gain of roughly 1–1.4%, showing a modest pickup in homebuying. The effective 30-year fixed rate eased to 6.76%, the lowest since early March, as inflation data and softer economic indicators bolstered rate-cut expectations. July’s core CPI rose 3.1% year-over-year, the highest since February, and—combined with weak labor data—pushed market odds for a September Fed cut to near 100%. The CME FedWatch Tool now shows a roughly 93–96% probability of a 25-basis-point cut, with analysts such as Goldman Sachs forecasting three cuts by year-end to bring rates toward a 3.00–3.25% target range. Overall, the rate pullback has prompted a wave of refinancing while home purchase demand edges higher, as the market positions for imminent Fed easing.

FedWatch: Target rate (in bps) possibilities, according to the CME Group (as of 08/14/2025 – 12:00 PM EST):

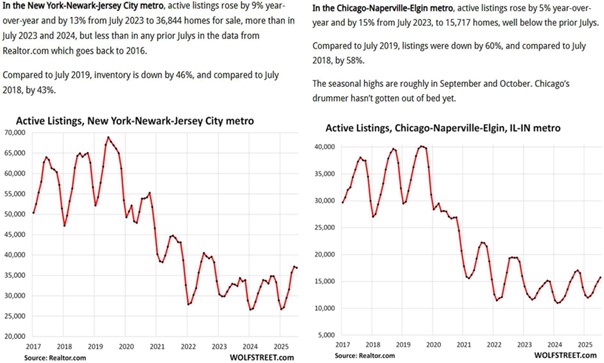

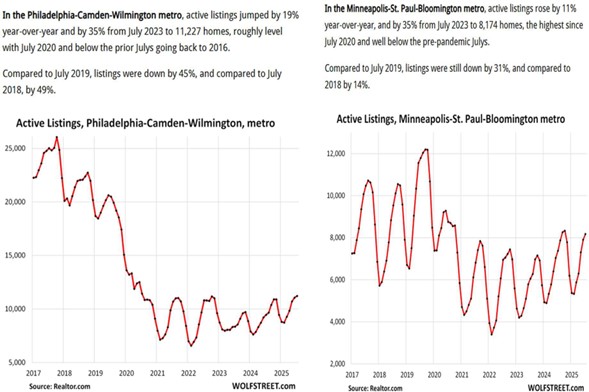

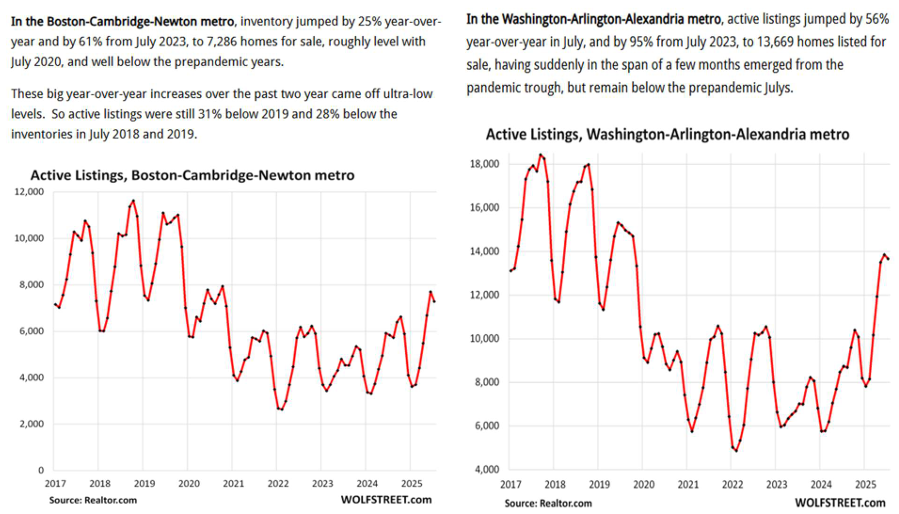

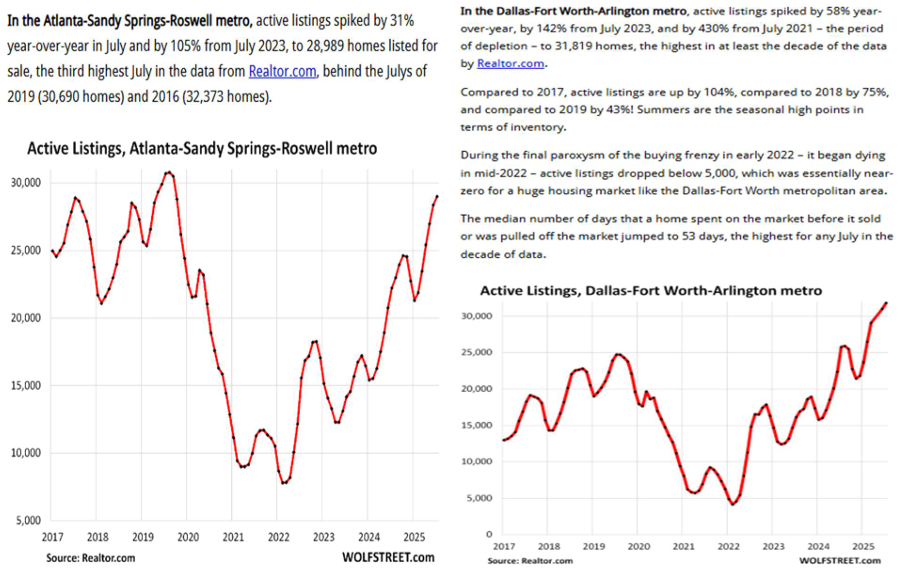

Inventory of Homes for Sale in Major Markets-Each market dances to a different drummer. But in some metros, the drummer hasn’t gotten out of bed yet.

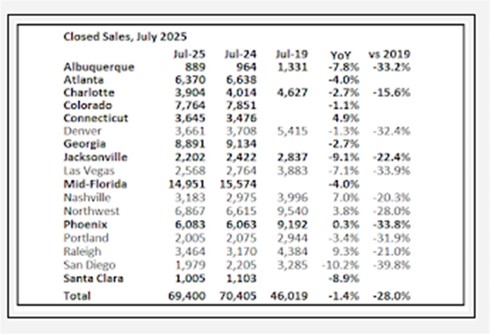

Closed Home Sales in 17 Housing Markets in July 2025

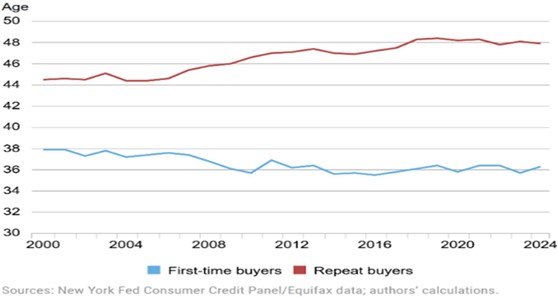

Average Age of First-Time Home Buyers and How it Changed over the Past 25 Years

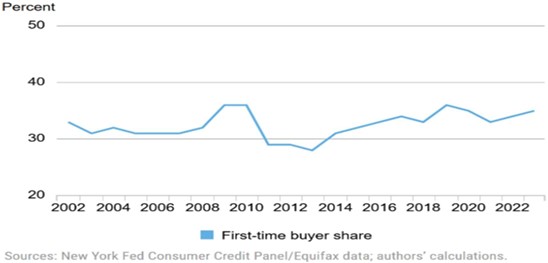

First-Time Homebuyers Are Also Making a Higher Share of all Home Purchases

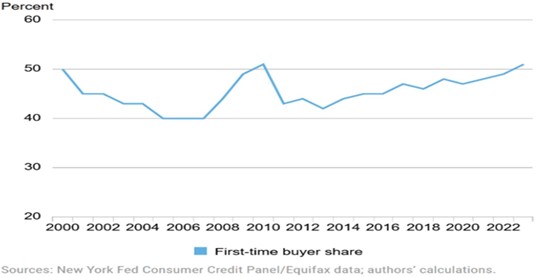

First-Time Homebuyers Share of Purchase Mortgages Has Been Improving

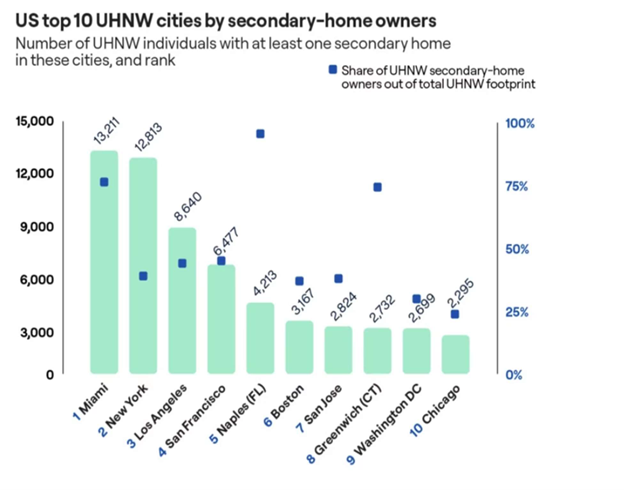

Where are the Ultra high net worth (UHNW) buying second homes?

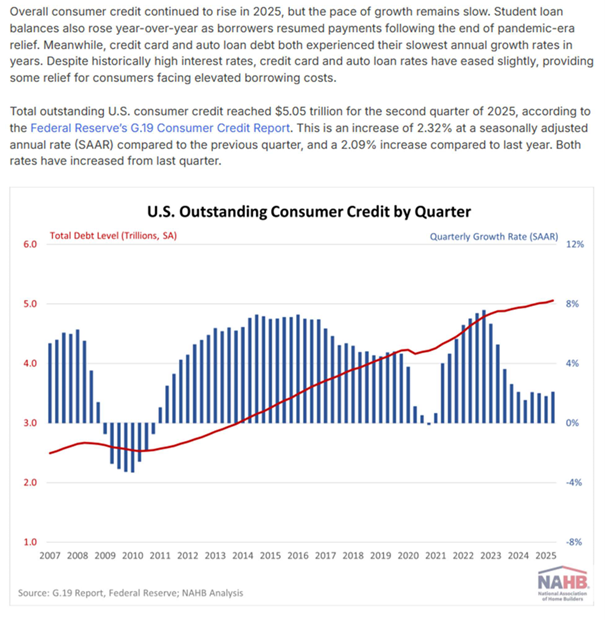

Outstanding Consumer Debt Balances

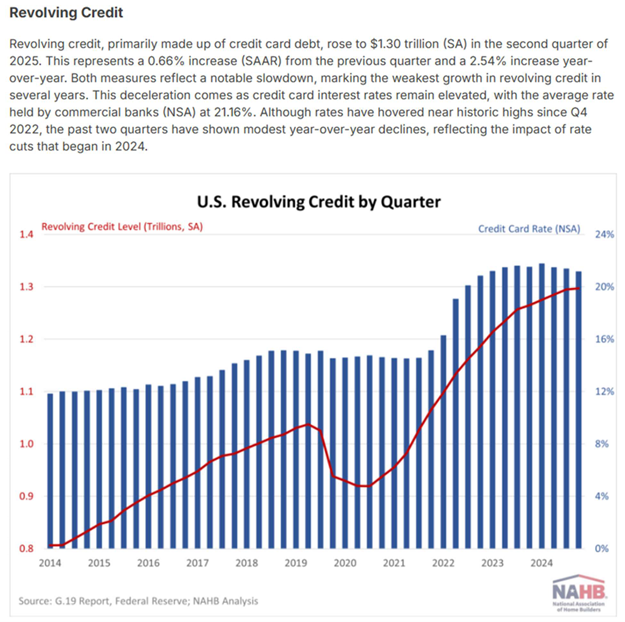

Credit Concern

During the month of June, outstanding credit card balances dipped $1.1 billion and that followed a $3.8 billion decline in May. Balances have now declined in three of the last four months, and over the past year credit balances have slipped $33 billion, or 2.5% Y-o-Y. This is a phenomenon we haven’t seen since spring 2021 and speaks to the cautious and frugal mentality being exhibited primarily by lower-end households. - Elliot F. Eisenberg the Bowtie Economist

*Communication is intended for Industry Professionals only and not intended for Consumer Distribution Interest rate and annual percentage rate (APR) are based on current market conditions as of 08/14/2025, are for informational purposes only, are subject to change without notice and may be subject to pricing add-ons related to property type, loan amount, loan-to-value, credit score and other variables. Estimated closing costs used in the APR calculation are assumed to be paid by the borrower at closing. If the closing costs are financed, the loan, APR and payment amounts will be higher. Contact us for details. Additional loan programs may be available. Accuracy is not guaranteed, and all products may not be available in all borrower's geographical areas and are based on their individual situation. This is not a credit decision or a commitment to lend. Actual interest rate, APR, and payment may vary based on the specific terms of the loan selected, verification of information, your credit history, the location and type of property, and other factors as determined by Prosperity Home Mortgage, LLC. Not available in all states. Rate is as of 08/14/2025 and is subject to change at any time without notice. Opinions, estimates, forecasts, and other views contained in this document are those of Freddie Mac’s economists and other researchers, do not necessarily represent the views of Freddie Mac or its management, and should not be construed as indicating Freddie Mac’s business prospects or expected results. Although the authors attempt to provide reliable, useful information, they do not guarantee that the information or other content in this document is accurate, current, or suitable for any particular purpose. All content is subject to change without notice. All content is provided on an “as is” basis, with no warranties of any kind whatsoever. Information from this document may be used with proper attribution.

.png)

.png)