This Market Update is written by our Capital Market specialists each week to bring you insight into what's happening in the market and how it may affect mortgage rates and real estate trends.

Market Commentary:

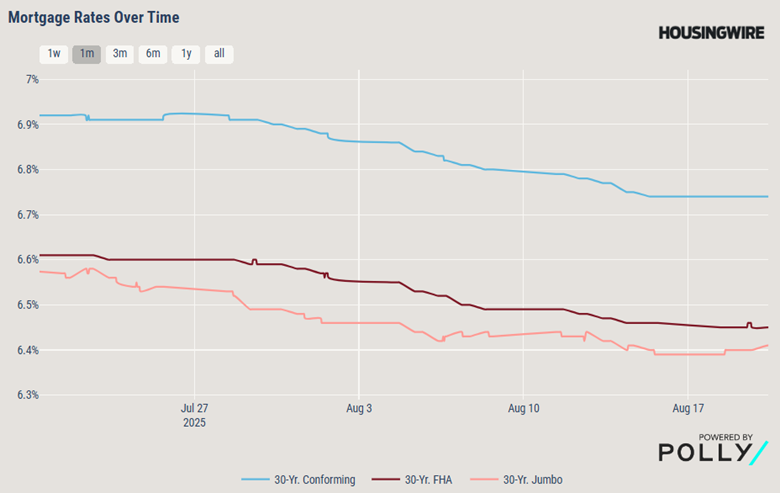

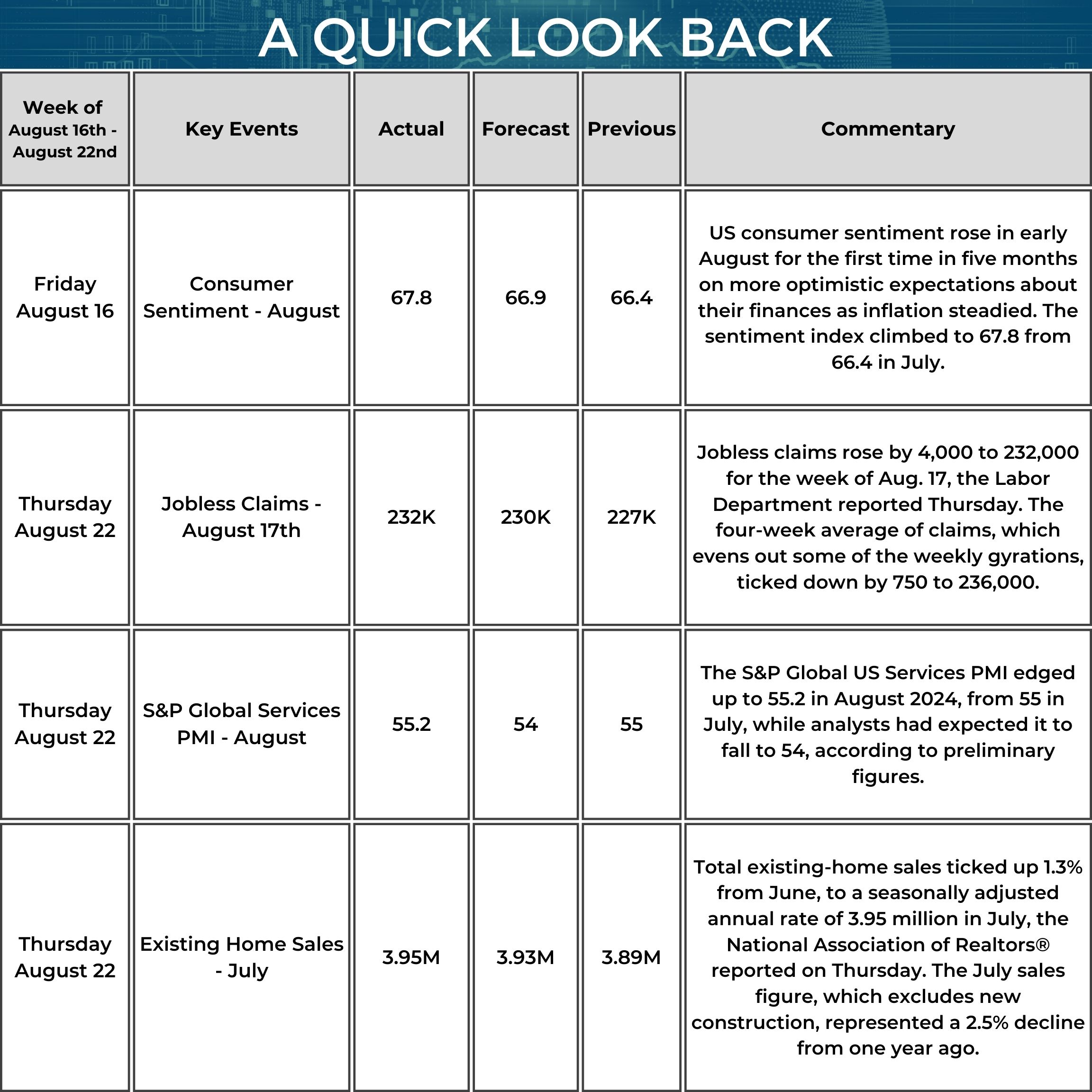

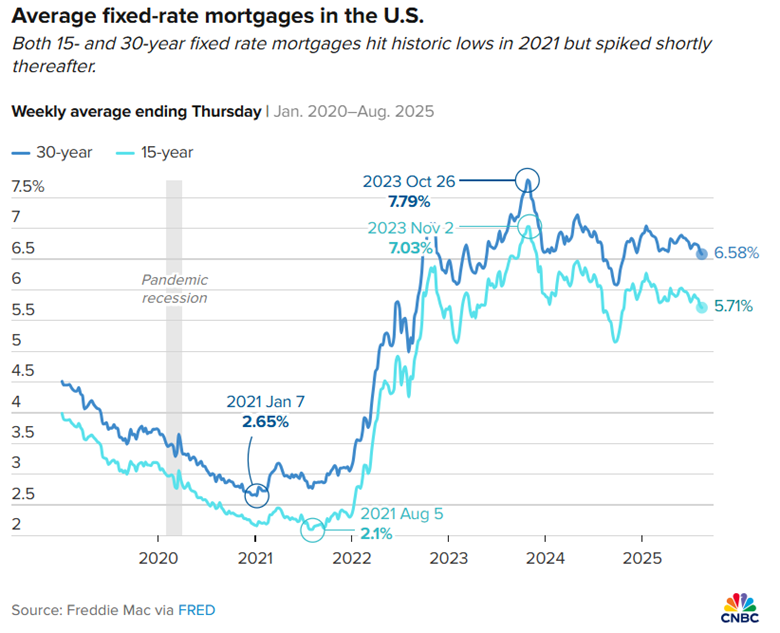

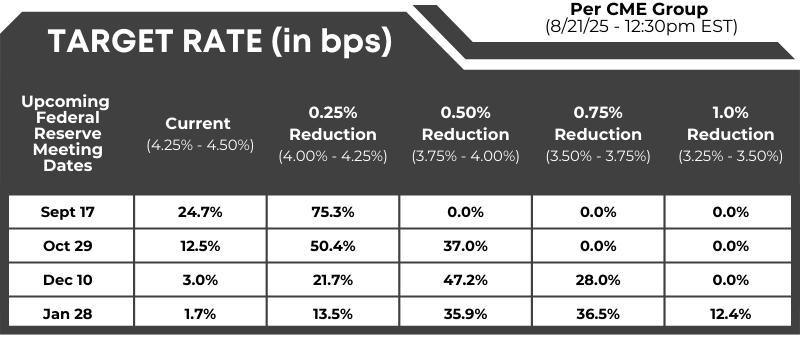

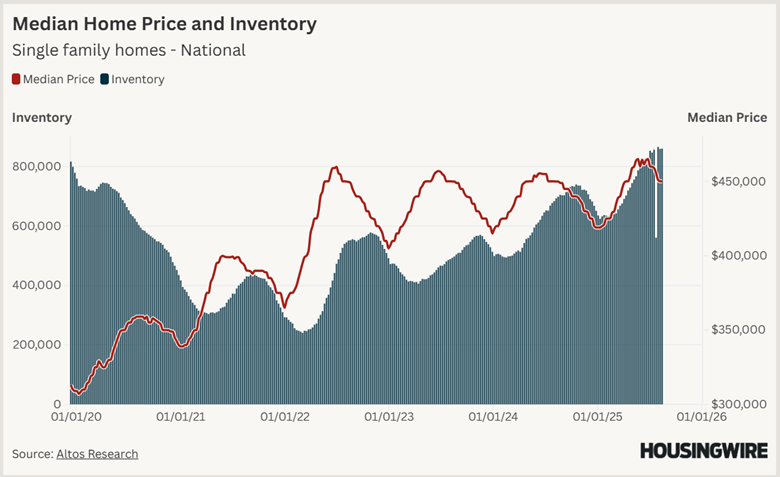

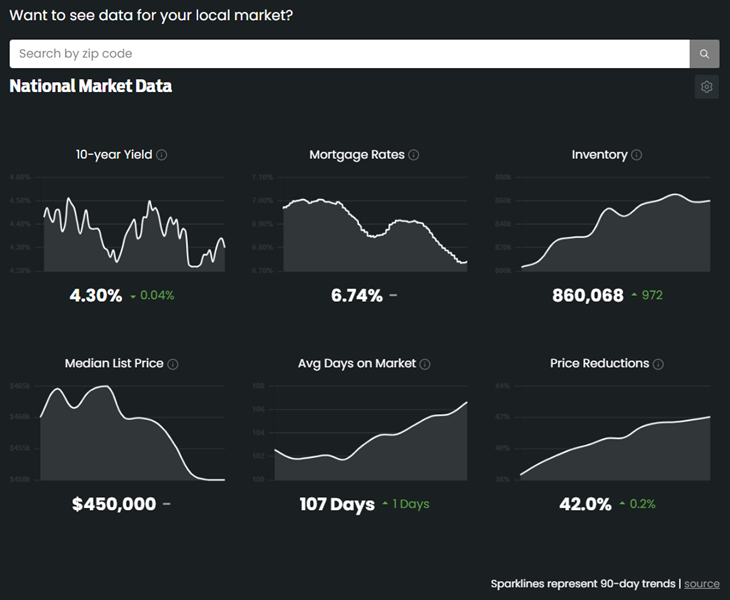

Between August 15 and August 21, 2025, mortgage rates edged slightly higher, with the 30-year fixed rate rising from to 6.74% on a 30 year fixed conforming loan, contributing to a 1.4% dip in mortgage applications. The August 20 FOMC minutes reinforced that most Fed officials still see inflation risks as outweighing labor concerns, signaling reluctance to cut rates further. On the consumer side, July’s Retail Sales Control Group rose 0.5%, showing resilience, but consumer sentiment disappointed, with the University of Michigan index slipping to 58.6 from 61.7 in July. Housing data was mixed: building permits climbed modestly to 1.354 million, and housing starts jumped5.2% to 1.428 million, driven by multifamily projects. However, builder confidence remains weak, with the NAHB Housing Market Index stuck in negative territory at 32, its 16th straight month below breakeven. Overall, the market reflects a tension between resilient spending and housing activity on one hand, and elevated mortgage rates, fragile builder sentiment, and a Fed still wary of easing policy on the other.

Fed Watch: Target rate (in bps) possibilities, according to the CME Group (as of 08/21/2025 – 12:00 PM EST):

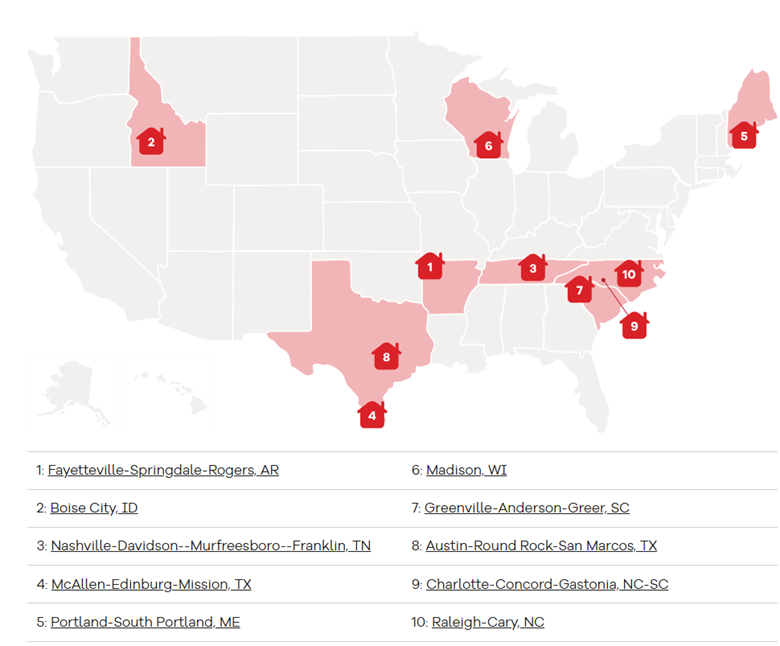

Where New Construction Thrives: Top Metros for 2025:

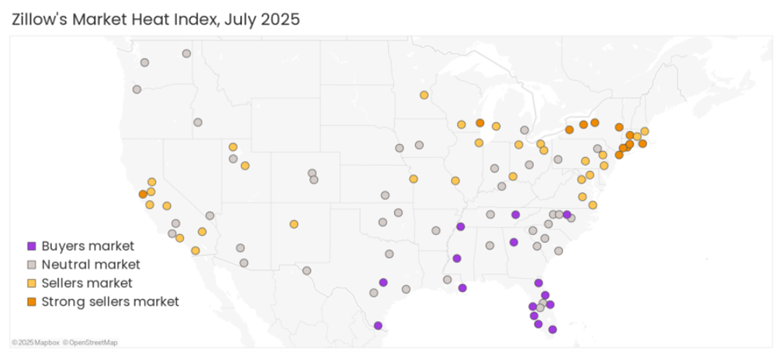

The Country’s Hottest Real Estate Markets Have Changed in 2025

Housing Market News and Commentary - HousingWire – interactive link

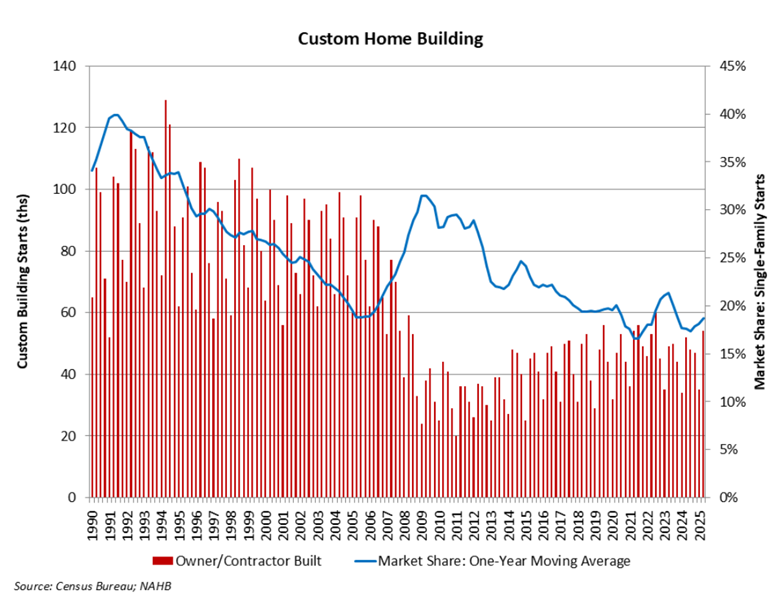

Growth for Custom Home Building

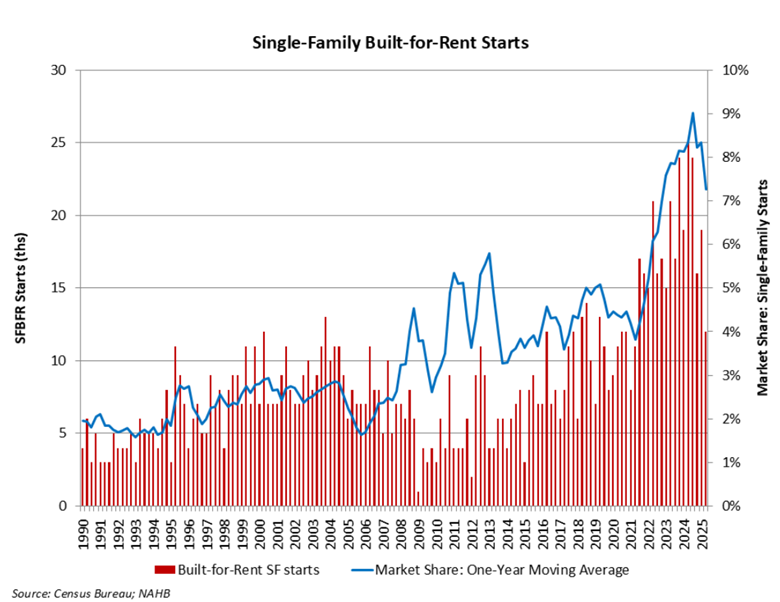

Retreat for Single-Family Built-for-Rent Housing

Pre-2015, wage growth was consistently higher for high-income workers than low-income ones. Starting in 2015, that began to reverse, and during Covid that new relationship was turbo-charged. Income growth for the bottom fifth of the population at times was twice as fast. Since late 2024, the old relationship as returned, with higher income earners gaining pay raises of roughly 1.5% to 2% more, a large amount, compared to the low-paid. - Elliot F. Eisenberg the Bowtie Economist

News You Can Use:

· Where Families Are Heading: Most Popular School Districts This Moving Season

· Mortgage rates are too high to get things moving again, says HousingWire's Logan Mohtashami

· DC home prices are still rising, but there’s a caveat skewing that headline - WTOP News

· The fever gripping the housing market seems to be breaking. Here’s why | CNN Business

· Dream of home ownership under threat as costs jump far past median incomes

· Senior living market can't keep up with demand as boomers age

· Mortgage rates hit a 10-month low: Why home buyers are on the sidelines

*Communication is intended for Industry Professionals only and not intended for Consumer Distribution. Interest rate and annual percentage rate(APR) are based on current market conditions as of 08/21/2025, are for informational purposes only, are subject to change without notice and may be subject to pricing add-ons related to property type, loan amount, loan-to-value, credit score and other variables. Estimated closing costs used in the APR calculation are assumed to be paid by the borrower at closing. If the closing costs are financed, the loan, APR and payment amounts will be higher. Contact us for details. Additional loan programs may be available. Accuracy is not guaranteed, and all products may not be available in all borrower's geographical areas and are based on their individual situation. This is not a credit decision or a commitment to lend. Actual interest rate, APR, and payment may vary based on the specific terms of the loan selected, verification of information, your credit history, the location and type of property, and other factors as determined by Prosperity Home Mortgage, LLC. Not available in all states. Rate is as of 08/21/2025 and is subject to change at any time without notice. Opinions, estimates, forecasts, and other views contained in this document are those of Freddie Mac’s economists and other researchers, do not necessarily represent the views of Freddie Mac or its management, and should not be construed as indicating Freddie Mac’s business prospects or expected results. Although the authors attempt to provide reliable, useful information, they do not guarantee that the information or other content in this document is accurate, current, or suitable for any particular purpose. All content is subject to change without notice. All content is provided on an “as is” basis, with no warranties of any kind whatsoever. Information from this document may be used with proper attribution.

.png)

.png)