This Market Update is written by our Capital Market specialists each week to bring you insight into what's happening in the market and how it may affect mortgage rates and real estate trends.

Market Commentary:

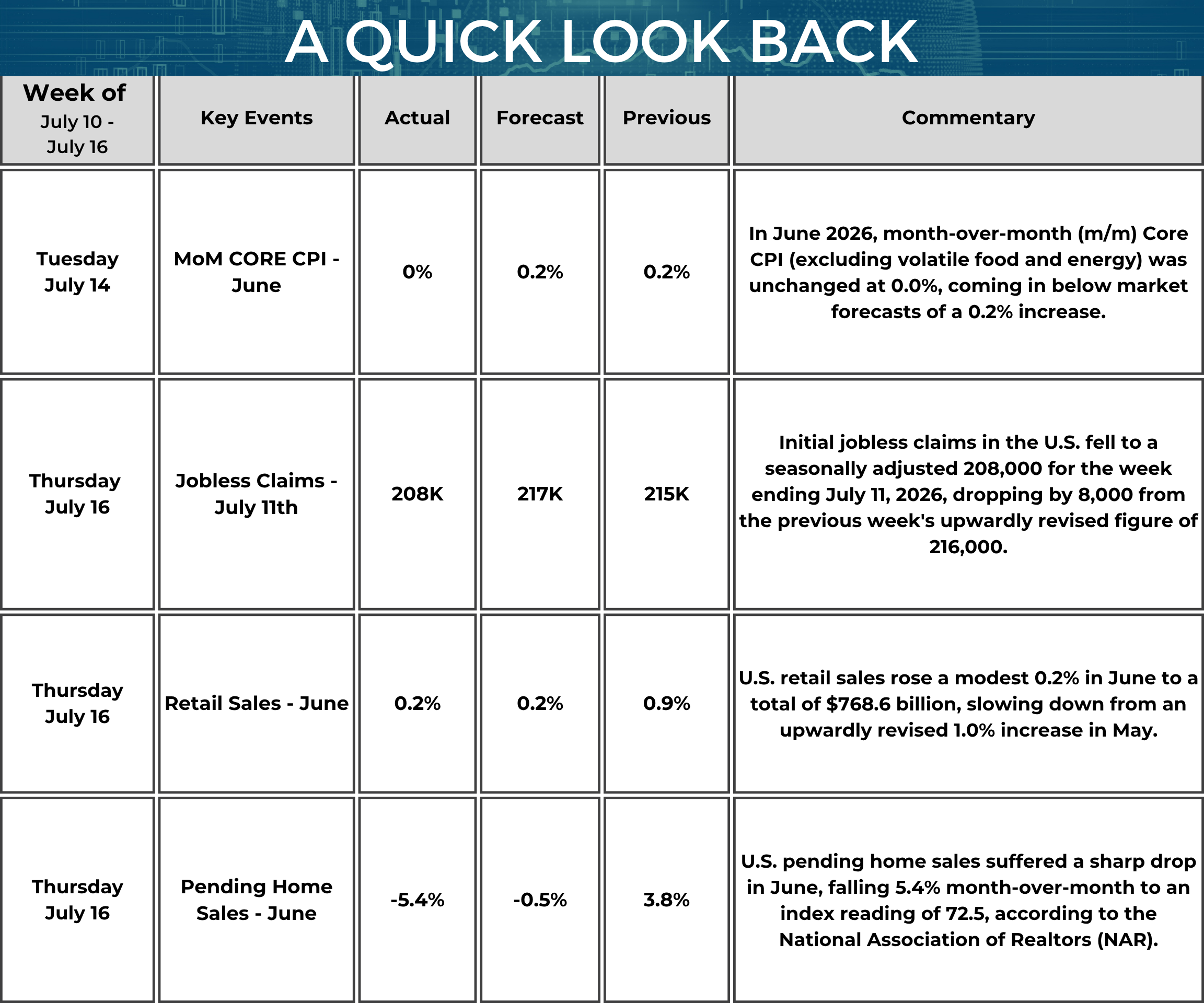

The primary catalyst driving this month’s mortgage market volatility is the benchmark 10-year U.S. Treasury yield, which has firmly retested the 4.56%–4.57% range. This upward pressure is fueled by a sticky core Consumer Price Index (CPI) hovering around 2.6% year-on-year, combined with fresh geopolitical energy shocks that have re-ignited broader inflation anxieties. Consequently, the bond market is aggressively pricing in a "higher-for-longer" monetary policy stance, making a Federal Reserve rate cut at the upcoming late-July meeting highly improbable. This macroeconomic backdrop has pushed the 30-year fixed mortgage rate to a near one-year high of 6.65%, introducing renewed friction into consumer affordability and pipeline velocity.

This climate requires shifting client conversations from macro timing to tactical advantages. The immediate byproduct of this rate surge is a 7.3% drop in the MBA purchase application index, hitting its lowest level since February. This contraction in aggregate demand represents a strategic window of execution for well-positioned buyers: reduced competition drastically increases buyer leverage, giving them the rare ability to negotiate price corrections or structural seller concessions.

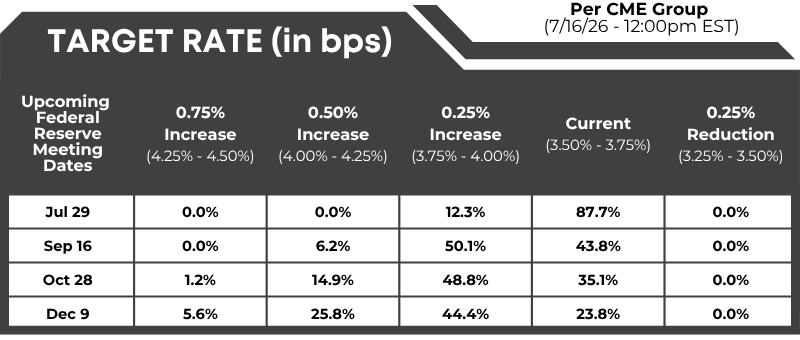

FedWatch: Target rate (in bps) possibilities, according to the CME Group (as of 07/16/2026– 12:00 PM EST):

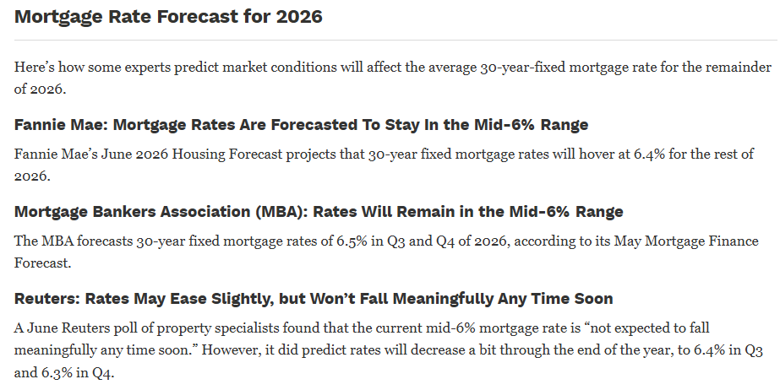

Mortgage Rates Forecast For 2026: Experts Predict Whether Interest Rates Will Drop:

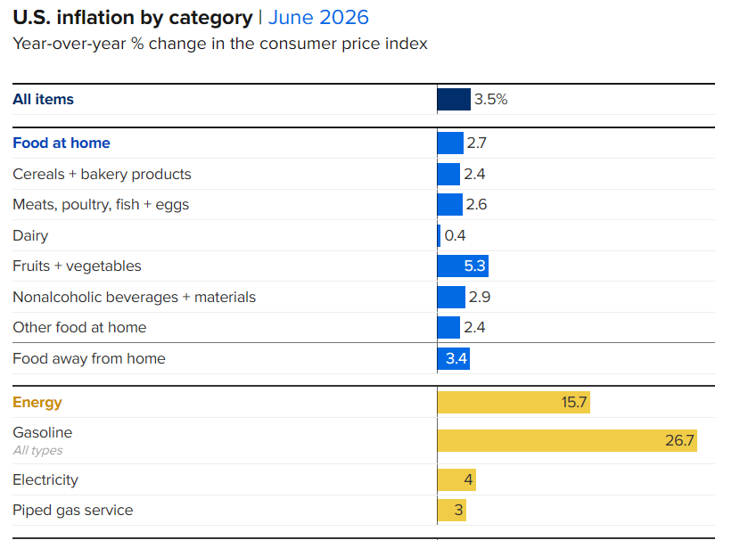

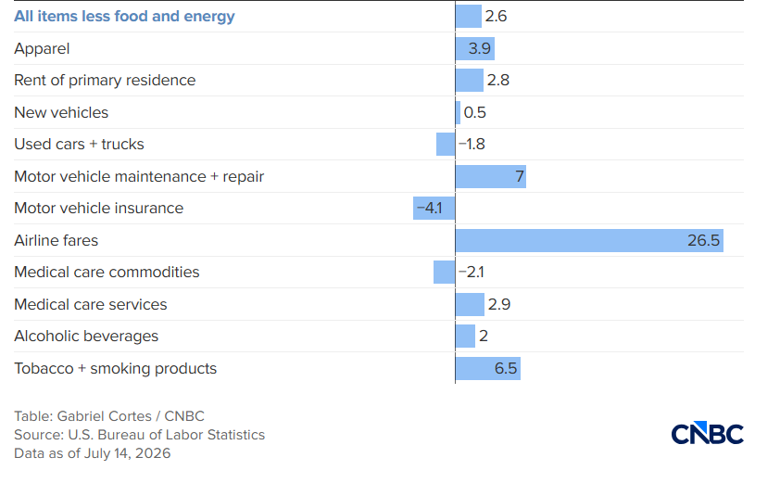

Here’s the Inflation Breakdown for June 2026

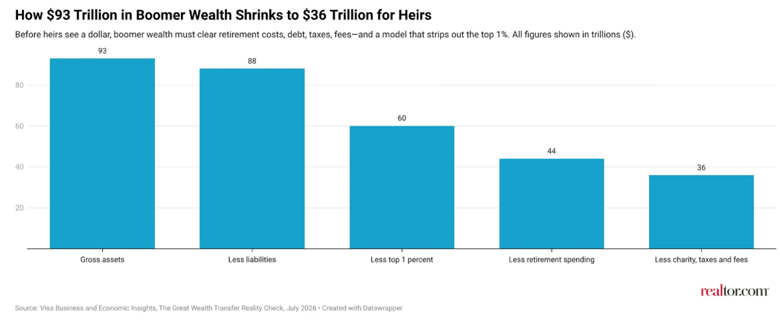

Boomers Hold $93 Trillion in Assets—but Their Heirs May Get Less Than Half

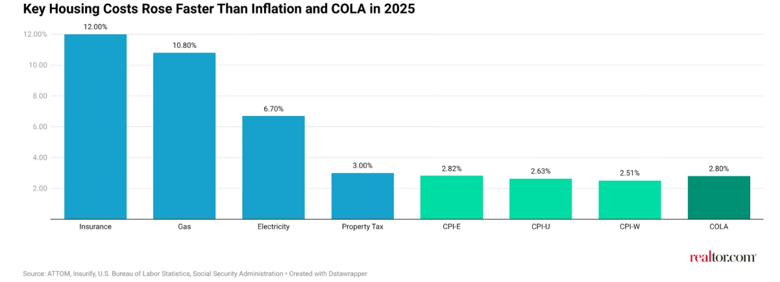

2027 Cost-of-living Adjustment(COLA) Projection Spikes to 3.8% in New Inflation Data

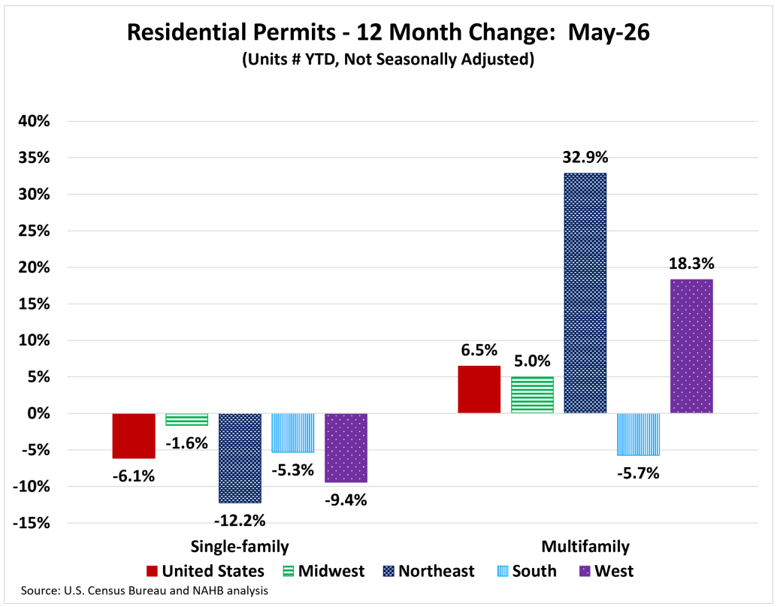

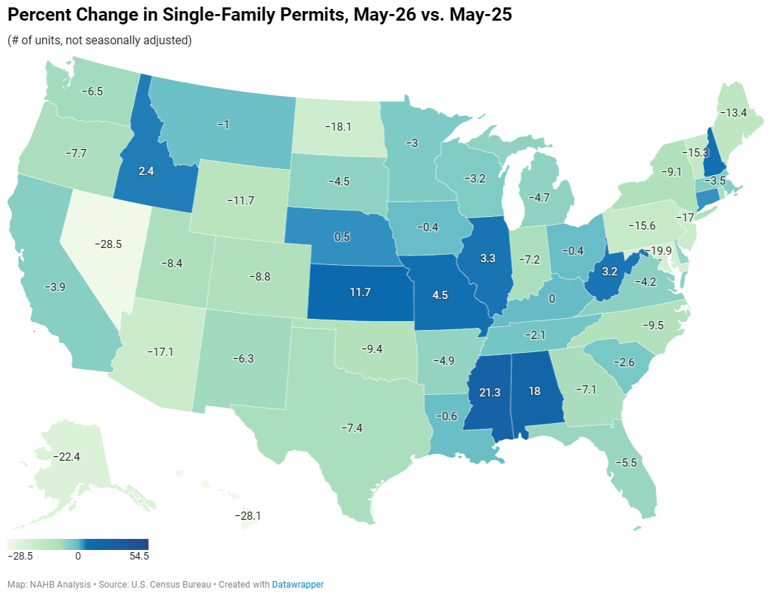

Single-Family Permitting Continued to Weaken Through May

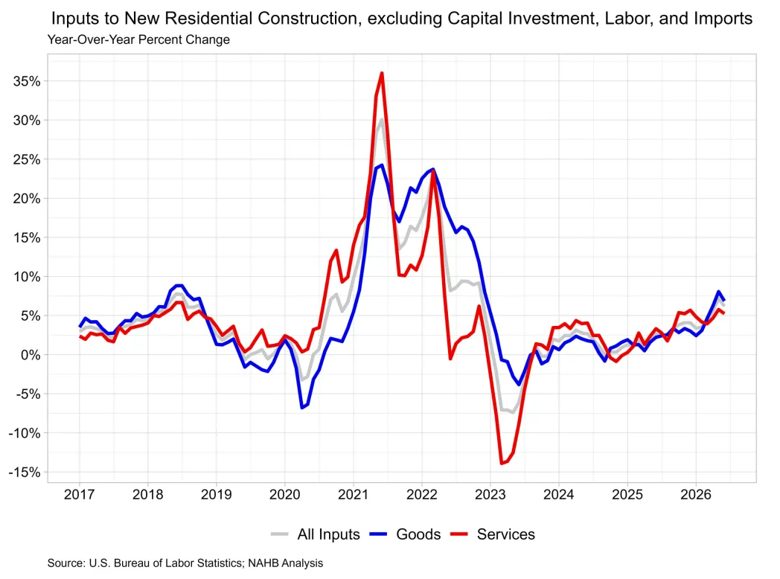

Building Material Prices Continue to Rise Despite Energy Price Declines

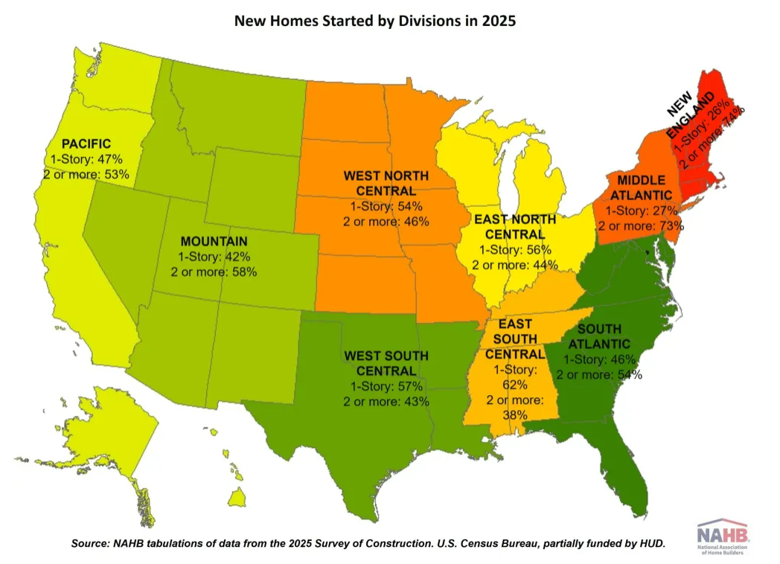

Two or More Story Home Starts Pull Back in 2025

Misallocation Malaise

While AI spending is boosting wages and driving massive investment in plant and equipment, it may, paradoxically, be reducing GDP growth. This is because AI spending is probably occurring much more quickly that it should be, like the Housing Boom. Due to this temporal misallocation of capital, other projects that at the margin would help the economy more get delayed or else never happen. AI is too much too soon. - Elliot Eisenberg, Economist

News You Can Use:

· Landmark Housing Bill Will Become Law Today, Without Trump

· Fed Beige Book: Growth Continues, Uncertainty Lingers

· New York Fed President Williams says inflation has peaked, rates 'well positioned'

· Consumer price index inflation report June 2026

· The 2026 Home Buying Season’s Fork in the Road (June 2026 Forecast) - Zillow Research

· NAR Pending Home Sales Report Shows 5.4% Decrease in June

*Communication is intended for Industry Professionals only and not intended for Consumer Distribution

Interest rate and annual percentage rate (APR) are based on current market conditions as of 07/16/2026, are for informational purposes only, are subject to change without notice and may be subject to pricing add-ons related to property type, loan amount, loan-to-value, credit score and other variables. Estimated closing costs used in the APR calculation are assumed to be paid by the borrower at closing. If the closing costs are financed, the loan, APR and payment amounts will be higher. Contact us for details. Additional loan programs may be available. Accuracy is not guaranteed, and all products may not be available in all borrower's geographical areas and are based on their individual situation. This is not a credit decision or a commitment to lend. Actual interest rate, APR, and payment may vary based on the specific terms of the loan selected, verification of information, your credit history, the location and type of property, and other factors as determined by Prosperity Home Mortgage, LLC. Not available in all states. Rate is as of 07/16/2026 and is subject to change at any time without notice. Opinions, estimates, forecasts, and other views contained in this document are those of Freddie Mac’s economists and other researchers, do not necessarily represent the views of Freddie Mac or its management, and should not be construed as indicating Freddie Mac’s business prospects or expected results. Although the authors attempt to provide reliable, useful information, they do not guarantee that the information or other content in this document is accurate, current, or suitable for any particular purpose. All content is subject to change without notice. All content is provided on an “as is” basis, with no warranties of any kind whatsoever. Information from this document may be used with proper attribution.

.png)

.png)