This Market Update is written by our Capital Market specialists each week to bring you insight into what's happening in the market and how it may affect mortgage rates and real estate trends.

Market Commentary:

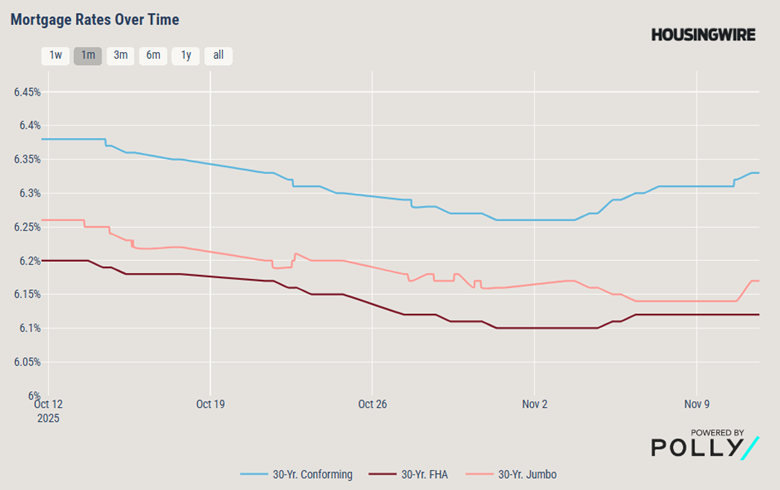

From November 7th to November 13th, 2025, interest rates remained stable, with no major changes from the Federal Reserve. Mortgage rates fluctuated slightly but continued their overall downward trend for the year. Market analysts continued to speculate about a potential rate cut in December, but Fed officials offered no clear signals as they remain divided: some emphasize inflation control, while others cite slowing job growth as a reason to ease.

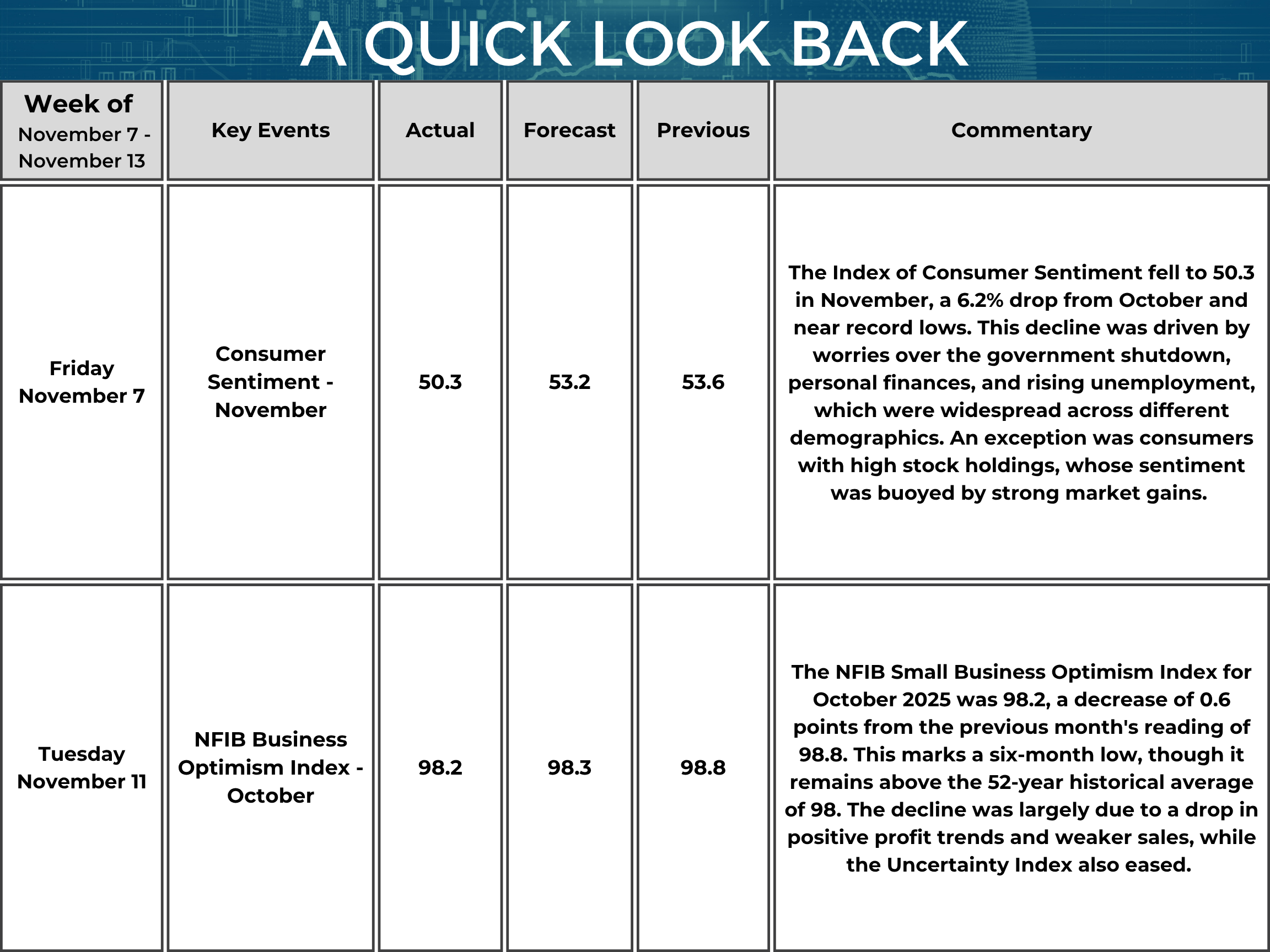

The Federal Reserve's policy committee meets next on Dec. 9 and 10, and officials are expected to cut the central bank's key interest rate to lower borrowing costs in an effort to stabilize the deteriorating job market. The Fed aims to stabilize the job market by lowering interest rates, but too many cuts too soon could stoke high inflation. The Fed faces a difficult balancing act in managing the risks of cutting too soon or too late.

The government shutdown that began Oct. 1 makes the Fed's decision more difficult because it has shuttered the government's statistical agencies. Without critical information about inflation and the job market, Fed officials have less to go on when deciding whether inflation or the job market is the more pressing problem to solve.

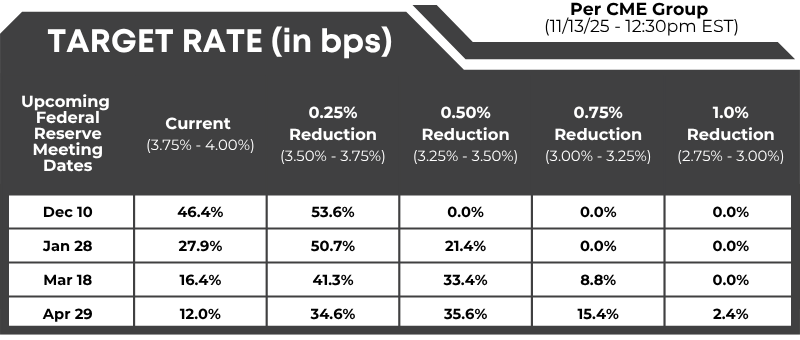

Fed Watch: Target rate (in bps) possibilities, according to the CMEGroup (as of 11/13/2025 – 12:00 PM EST):

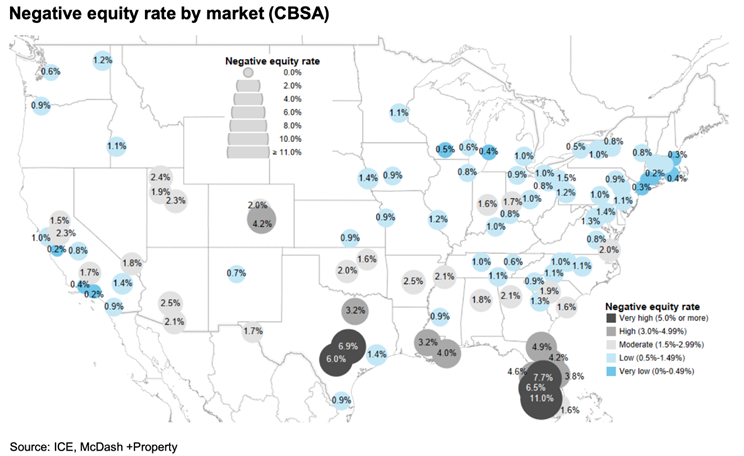

Negative Equity Rates Have Increased:

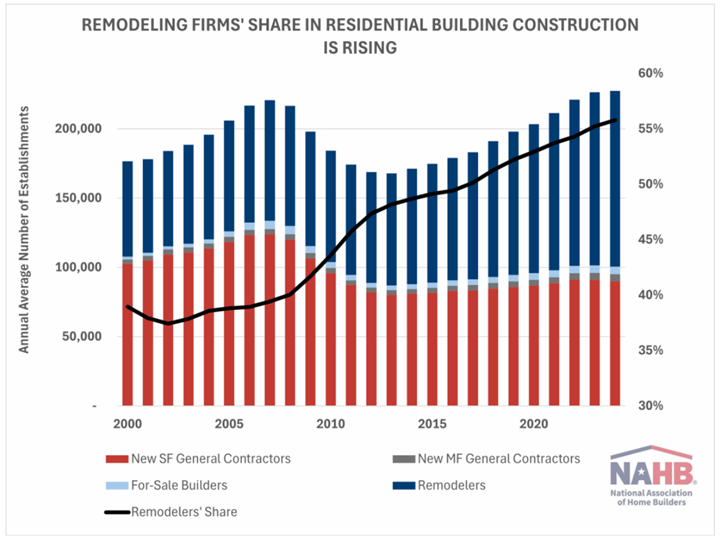

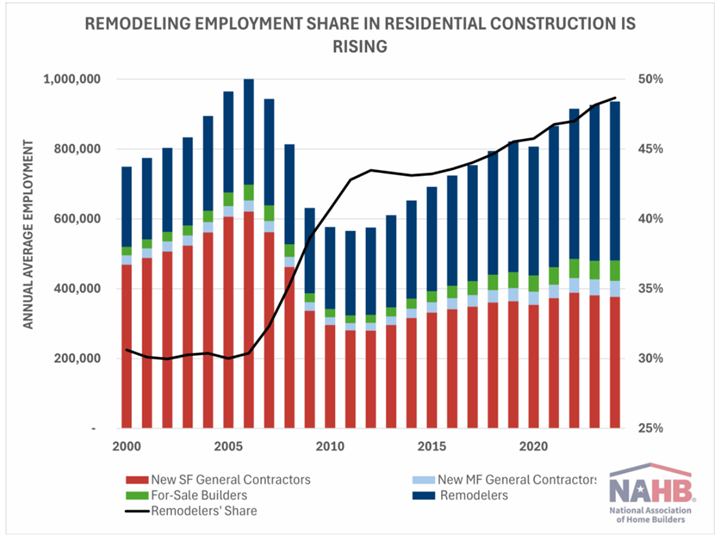

Remodelers on the Rise: How Renovation is Reshaping Residential Construction:

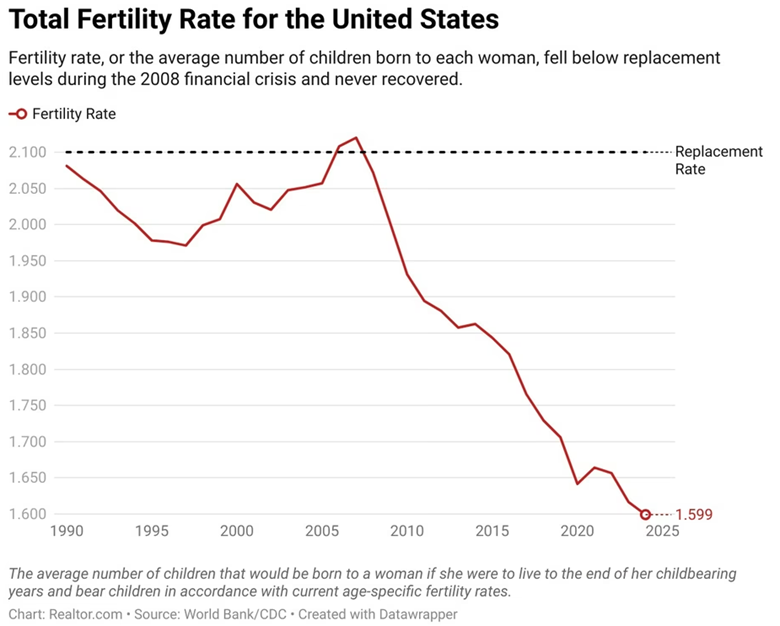

Rising Housing Costs Are Main Reason for Falling U.S. Fertility Rates, Study Finds:

Mortgage Madness:

There’s now talk of 50-year mortgages. Bad idea. First, with the median age of first-time buyers 40, borrowers would likely never pay off their mortgage. Second, the difference between a 10-year mortgage and a 30-year mortgage is 65bps, the gap between the 30-year and 50-year mortgage will also be sizable. Absent a deep secondary market for 50-year mortgages, investors will be reluctant lenders. Lastly, easier financing just raises prices.- Elliot Eisenberg, Economist

News You Can Use:

· Boston Fed President Collins advocates holding rates steady, sees ‘high bar’ for further cuts

· Mortgage demand from homebuyers hits highest level since September

· Government Reopens After Record Shutdown: What It Means for Housing

· Fannie Mae and MBA agree: Most of the mortgage rate relief is already behind us

· Should You Buy a House Now or Wait Until 2026?

· November ICE Mortgage Monitor: Home Prices "Firmed" in October, Up 0.9% Year-over-year

· Would a 50-year mortgage make home ownership attainable?

· Luxury Real Estate Market Set To Reach $338 Billion by 2030

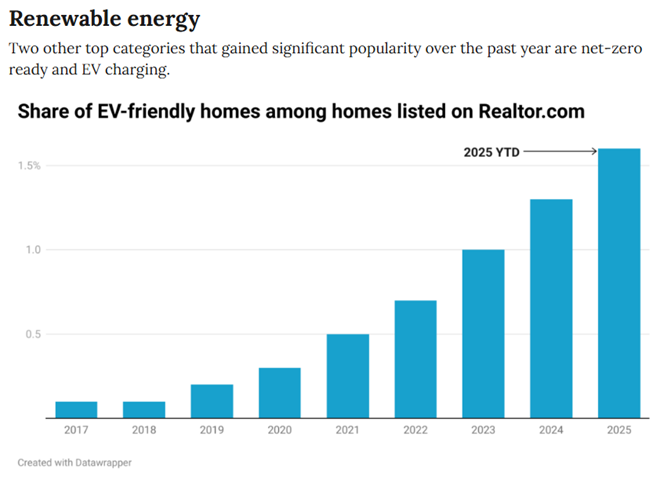

· Hottest Home Trends in 2025 - Realtor.com Economic Research

*Communication is intended for Industry Professionals only and not intended for Consumer Distribution

Interest rate and annual percentage rate (APR) are based on current market conditions as of 11/13/2025, are for informational purposes only, are subject to change without notice and may be subject to pricing add-ons related to property type, loan amount, loan-to-value, credit score and other variables. Estimated closing costs used in the APR calculation are assumed to be paid by the borrower at closing. If the closing costs are financed, the loan, APR and payment amounts will be higher. Contact us for details. Additional loan programs may be available. Accuracy is not guaranteed, and all products may not be available in all borrower's geographical areas and are based on their individual situation. This is not a credit decision or a commitment to lend. actual interest rate, APR, and payment may vary based on the specific terms of the loan selected, verification of information, your credit history, the location and type of property, and other factors as determined by Prosperity Home Mortgage, LLC. Not available in all states. Rate is as of 11/13/2025 and is subject to change at any time without notice. Opinions, estimates, forecasts, and other views contained in this document are those of Freddie Mac’s economists and other researchers, do not necessarily represent the views of Freddie Mac or its management, and should not be construed as indicating Freddie Mac’s business prospects or expected results. Although the authors attempt to provide reliable, useful information, they do not guarantee that the information or other content in this document is accurate, current, or suitable for any particular purpose. All content is subject to change without notice. All content is provided on an “as is” basis, with no warranties of any kind whatsoever. Information from this document may be used with proper attribution.

.png)

.png)